Artificial Intelligence has indeed changed considering the parameters in which lenders have operated to determine creditworthiness they are faster, sharper and perhaps more objective than before. In the past, checking a person's financial reliability involved a lot more manual check-up, long documentation, and even sometimes prejudice in human judgment. In contrast, AI powered applications can analyze thousands of variables in seconds, from spending patterns and repayment histories to more subtle behavioral patterns. This makes for less time over which a decision is made on the loan but also more uniformity and accuracy with which applicants are considered. Process becomes less personal in the sense that it's devoid of emotional influence; instead, the process relies on data-driven insights. Borrowers would receive responses more quickly, and lenders would minimize the risk of errors or subjective favoritism. In short, it has turned credit scoring into a very accurate, speedy, and mostly impartial science that weighs fairness against speed so that both financial institutions and decent borrowers would benefit.

How AI Improves Credit Scoring

All the while historical credit systems are based on old-fashioned data systems for example past loans, repayment records, and credit card usage. Although those data are usually used in classic scoring, they cannot adequately explain the financial well-being of an individual. It paints a picture of someone with probably high risk, although has been monitored on a monthly basis as well as maintaining savings, a more likely person without a credit card and a formal loan record. Artificial Intelligence is a revolution because AI models can analyze far more than judging with the old-fashioned scoring systems. They could monitor spending patterns such as these- rent and utility payments; subscription renewals; activity in digital wallets; little known transactions that have previously been neglected; and even microtransactions. Some are beginning to employ alternative repositories such as consistency in mobile phone payments, histories of e-commerce purchases, and behavioral aspects with money in social financial networks. Thus, people can have access to speedier and more inclusive decisions when combined with an AI hitting into the myriad heterogeneous streams comprising real-time data records. Those who were previously unable to access the credit markets-regions such as fresh, young professionals to freelance and those in emerging markets-can also demonstrate prudent financial management in an alternative way where former traditional scores failed. This indeed creates a fairer, more representative system to offer what people actually are doing with today's internet-first economy.

Faster Loan Approvals

The lending process, however, is undergoing monumental changes due to AI led underwriting that permissionning instant risk evaluation and loan approval within a matter of hours. By contrast, underwriting would traditionally take several days often, weeks involving manual scrutiny of income documents, employment history, credit reports, and supporting papers. This caused not only delays and inefficiencies on the part of banks and financial institutions but also very moments of impatience on the part of the borrower, who craved quicker resolutions. Risk assessment with AI, however, is conducted in real-time. AI models can analyze a myriad of data points from traditional credit history to digital spending patterns and sources of alternative data to create a risk profile within minutes. In comparison, it is astonishing how much faster and accurately these machine-learning algorithms highlight the patterns invisible to human eyes and predict the likelihood of repayment. These changes represent a turnaround for banks and clients alike. For financial institutions, the cost of running the business and time stuck in paperwork are reduced, freeing human brains to better use for high-value decision-making and customer service. For borrowers, everything seems to operate smoothly: loan approval that formerly could take weeks can now occur within minutes, right in line with today's fast-paced digital world. This efficiency increases customer satisfaction and deepens trust in the institution because those borrowers feel valued and cared for through fair and timely decision-making. In many ways, AI has raised the bar and turned what used to be a bitter process into a lenders' competitive advantage.

Reducing Human Bias

The lending process, however, is undergoing monumental changes due to AI led underwriting that permissionning instant risk evaluation and loan approval within a matter of hours. By contrast, underwriting would traditionally take several days often, weeks involving manual scrutiny of income documents, employment history, credit reports, and supporting papers. This caused not only delays and inefficiencies on the part of banks and financial institutions but also very moments of impatience on the part of the borrower, who craved quicker resolutions. Risk assessment with AI, however, is conducted in real-time. AI models can analyze a myriad of data points from traditional credit history to digital spending patterns and sources of alternative data- to create a risk profile within minutes. In comparison, it is astonishing how much faster and accurately these machine-learning algorithms highlight the patterns invisible to human eyes and predict the likelihood of repayment. These changes represent a turnaround for banks and clients alike. For financial institutions, the cost of running the business and time stuck in paperwork are reduced, freeing human brains to better use for high-value decision-making and customer service. For borrowers, everything seems to operate smoothly: loan approval that formerly could take weeks can now occur within minutes, right in line with today's fast-paced digital world. This efficiency increases customer satisfaction and deepens trust in the institution because those borrowers feel valued and cared for through fair and timely decision-making. In many ways, AI has raised the bar and turned what used to be a bitter process into a lenders' competitive advantage.

Stay Updated with Cenvexa

Get the latest insights on personal finance and money management delivered to your inbox.

Subscribe to Our NewsletterYou might also like

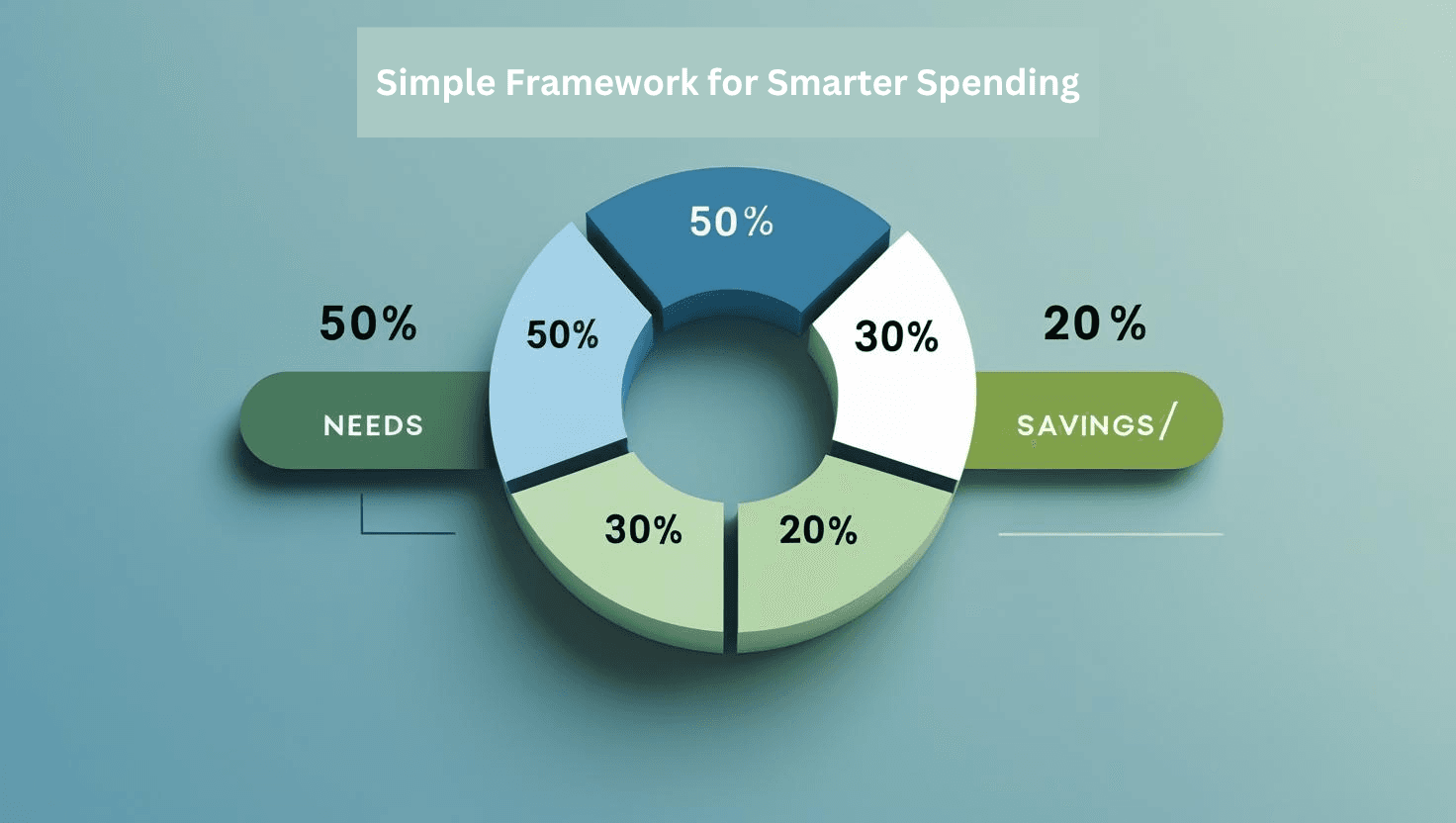

The 50/30/20 Rule: A Simple Framework for Smarter Spending

Arpan Paul

September 20, 2025

Zero-Based Budgeting: How to Make Every Rupee Work for You

Arpan Paul

September 20, 2025

Goal-Based Money Management: Attain Financial Milestones Quickly

Arpan Paul

September 20, 2025